Register for Payroll Tax

If you pay taxable wages in the ACT and you pay (or your group pays) monthly Australia-wide wages that exceed the ACT’s monthly threshold, you have to register for payroll tax in the ACT. By law, you must apply to register within 7 days after the end of the month that you go over the threshold amount.

As of 1 July 2016, the ACT’s monthly threshold is $166,666.66 per month.

How to register for payroll tax

To register, use the Online Payroll Tax Registration - Notification form.

In addition to new registrations, you can also use this form to:

- reactivate a registration

- notify the ACT Revenue Office of any changes to your circumstances

- cancel your registration.

For more information, see the Registration for ACT Payroll circular (PTA071.1).

How your employer status affects the way you lodge

Example of a grouping matter

Example of a grouping matter

Company A Pty Ltd - JRL/DGE/GM

Company B Pty Ltd - GM

Company C Pty Ltd - GMLI

In the above example, Company A Pty Ltd is the JRL and will lodge for itself and Company B Pty Ltd. This means Company B Pty Ltd does not lodge returns with the ACT Revenue Office. Company A Pty Ltd will lodge and include Company B Pty Ltd's wages and claim the threshold on their combined wages.

Company C Pty Ltd is still required to lodge returns with the ACT Revenue Office and will be charged at the flat rate of 6.85%.

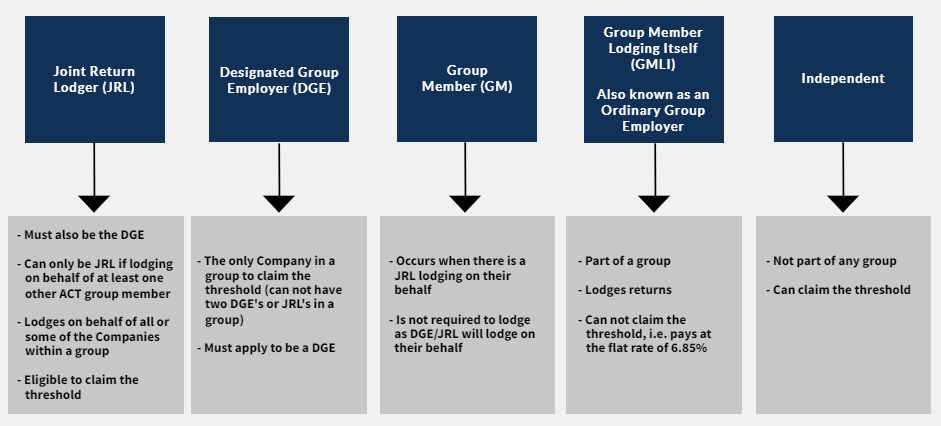

What is my employer status?

When registering for payroll tax and lodging returns, you must declare your employer status. Your employer status relates to whether you are or are not part of a group, and affects your ability to claim the threshold, and how much of the threshold you can claim.

The 3 Employer Status Categories are:

An independent is not part of a payroll tax group and is entitled to claim the threshold.

As only one member of a group is allowed to claim the threshold, the members of the group can nominate one member to claim the payroll tax threshold. This is known as the Designated Group Employer (DGE). The DGE must be approved by the Commissioner.

A group may elect for the DGE to lodge a Joint Return on behalf of particular or all group members. In this instance, the DGE is known as a Joint Return Lodger (JRL). Where a DGE is a JRL, all members taxable wages are recorded on the one return and this member is entitled to claim the threshold. Only an approved DGE can apply to be a JRL.

Those members of the group included in a JRL nomination are not required to lodge monthly and annual returns. All other taxpayers who form part of the group, but are not included in the JRL nomination, are required to lodge monthly and annual returns as an Ordinary Group Employer.

Is an employer who pays taxable wages in the ACT and is part of a group. An Ordinary Group Employer is not allowed to claim the threshold and payroll tax is calculated at the relevant rate multiplied by their ACT taxable wages.

What happens if you declare the wrong Employer Status?

Incorrectly declaring your employer status, or not disclosing all members of your group, may result in your business over-paying or under-paying its payroll tax liability. Where you under-pay your payroll tax liability, depending on the circumstances and nature of the tax default, the Commissioner may apply penalty tax and interest.

For Example:

- Smith & Co Pty Ltd declared they only operate in the ACT and paid $3 million in wages per financial year.

- Smith & Co Pty Ltd lodged payroll tax returns and self-assessed themselves as an independent employer for 3 years claiming the full tax free threshold of $2 million.

- Based upon their self-assessment and lodgements as an independent employer, Smith & Co Pty Ltd paid $68,500 in ACT payroll tax per year.

- As a result of a compliance investigation it was determined Smith & Co Pty Ltd is part of a group with a number of businesses within Australia, however Smith & Co Pty Ltd is the only group member paying taxable wages in the ACT.

- The Commissioner determined, due to the Australia wide wages of Smith & Co Pty Ltd’s group members ($12 million), that Smith & Co Pty Ltd was only allowed to claim 25% of the payroll tax threshold.

- The Commissioner determined Smith & Co Pty Ltd underpaid their ACT payroll tax by $308,250 for 3 years and charged penalty tax and interest on the underpaid tax.